CHG Issue #226: How Empires Fall

Both Trump and Xi see opportunity in the upcoming meeting and rebalancing power around their countries and the stakes couldn't be higher

We went back and reread our 2025 Macro Story and found it notable that outside of oil not much has changed for the markets this year despite the outbreak of war in the Middle East. This can mean many things, and we aren’t going to cover them all, but we are going to focus on the money flows because it is better to listen to where people are placing their bets versus what they are saying.

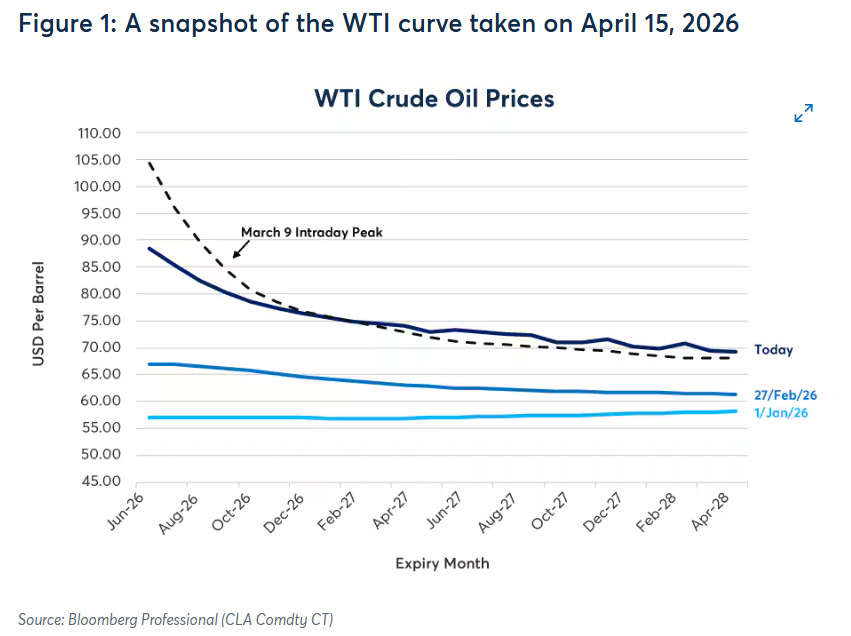

The market has consistently priced the oil curve in backwardation. This could be because the market thought the war would end quickly, that producers would find a way around Hormuz (ex. UAE exiting OPEC), or the market was just overly optimistic about TACO. Regardless of the reason, the pricing is notable since the IRGC have made control of the Strait the central element of their strategy and the US has struggled to reopen the waterway. Control of the Strait is now an existential issue for the IRGC, and they will likely go to extreme measures to ensure their survival.

Given the stakes for the IRGC and the West’s inability to reopen the waterway it would make sense to price in more of a long-term disruption, but the market continues to undermine the IRGC’s position by only pricing in a short-term spike in oil prices. Maybe the market knows that it is highly unlikely that the IRGC can sustain the current status quo. Either through an economic crisis that results in widespread and uncontrollable civil unrest or western powers slowly prying open shipping lanes, the time is not on the IRGC’s side.

Additionally, their erstwhile allies Russia and China have interests and dealings of their own with the West that are not necessarily aligned with the IRGC. China remains heavily dependent on access to not only oil flowing through the Strait but also US markets and ultimately the US is of far greater concern for China than Iranian oil.

Russia has been actively approaching the US over the past two weeks, a notable change from the past, as its economy is facing intensifying strain and it sees its influence being marginalized as the US and China move closer together. Russia has a lot to lose from the upcoming Trump-Xi summit which could see Russia further marginalized if Beijing and Washington can emerge with a new understanding. Therefore, Putin and Lavrov both reached out to their counterparts in Washington last week to talk.

In these moves we see an outcome of Washington’s strategic shift to deal with adversaries independently. The shift is exposing the incoherence of the anti-US alignment between Iran-Russia-China because it exploits the distinct vulnerabilities of each. For the IRGC-led regime in Tehran the imperative is regime survival, but Moscow is seeking a satisfactory end to the Ukraine war and relieve pressure on its economy, and Beijing is attempting to counterbalance and undermine US hegemony wherever it can. Therefore, it is entirely possible to see a negotiated settlement where a weakened IRGC without strong backing from Russia is pressured by an oil-dependent China to give up control of the Strait.

We must be careful not to use this to justify market pricing but only to consider what the market might be really saying. Backwardation is not unusual in this sort of environment, but it has been consistently highlighted by a broad array of talking heads during this whole affair. If China was really worried about their access to Iranian oil they would be bidding up long-dated oil futures; their size would overwhelm the back end of the curve. But this is not happening.

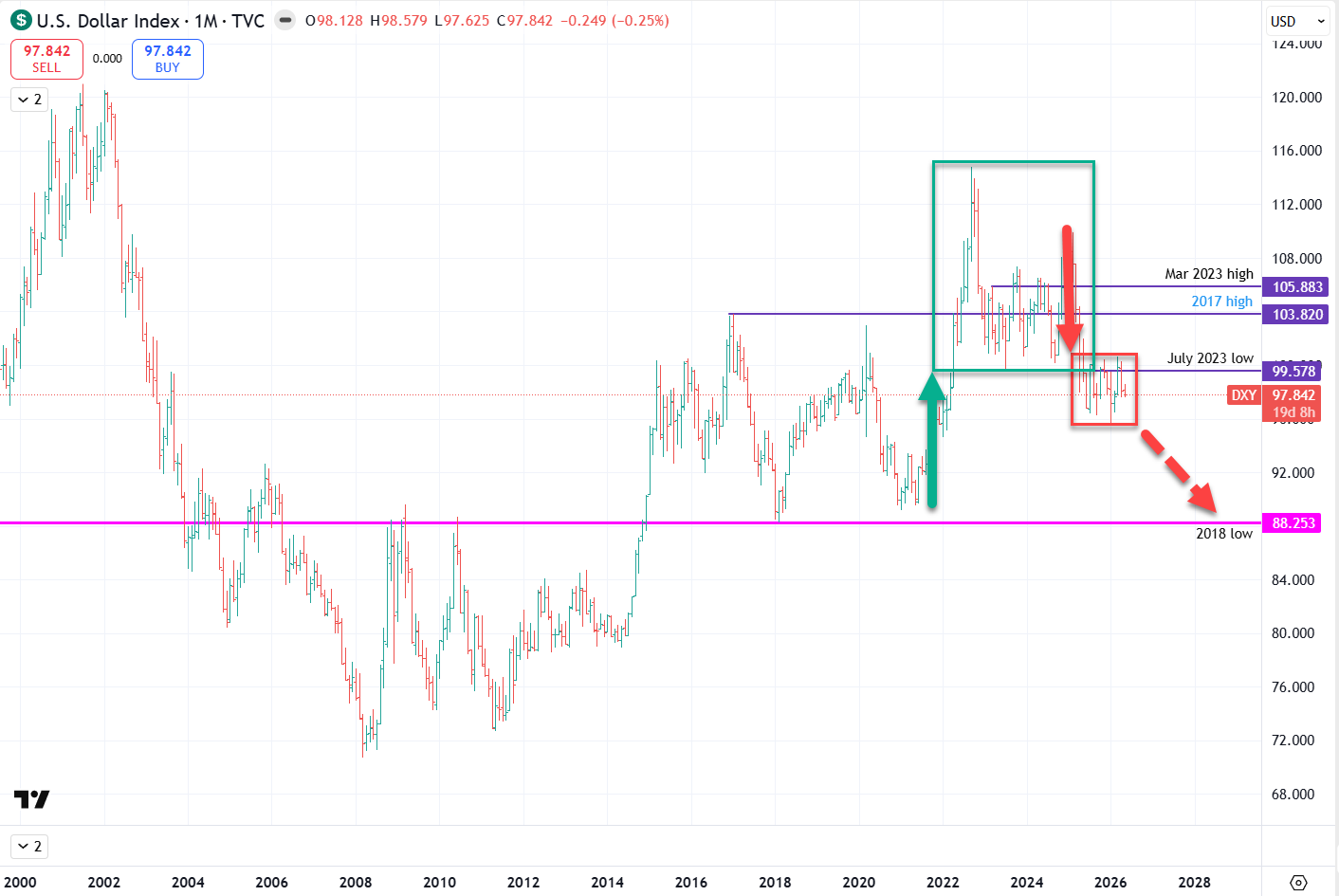

Another anomaly that has caught our attention is that the dollar is not rallying. The market has worked off the long inventory from the 2022-2023 rate hike rally and we would have expected the war to provide the catalyst for the DXY to find acceptance back above the 2023 low and retest the 2017 high but that has not happened.

What is going on here? Part of the impetus for the “America First” strategy is a recognition that the dollar’s reserve currency status has weakened America by hollowing out its manufacturing core and allowed the government to run irresponsible deficits, accumulating a dangerous amount of debt. This is how reserve currencies die; the US sees it happening and is trying to prevent it.

But it’s not just US strategy that is driving this anomaly, the AI boom is leaving its mark in some unconventional ways.

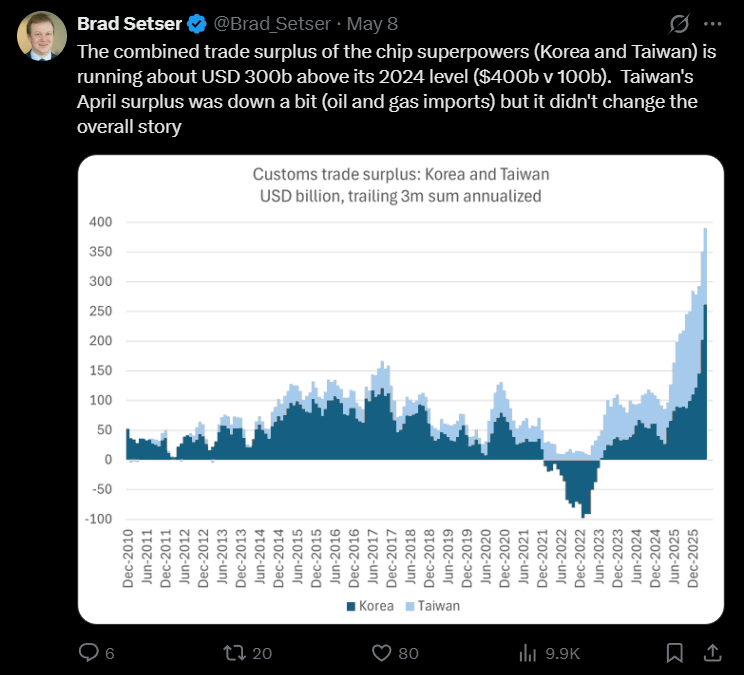

It’s wild to consider that the AI capex boom has increased Korea and Taiwan’s trade surplus by $300B, their currencies remain historically weak, and the USD has remained under pressure. Normally foreign exporter surpluses flow back into dollars via reserve bond purchases which would offset the outflows from AI capex spending, but today those surpluses are being recycled into equities which reduces US bond purchases, putting upward pressure on US rates, and putting downward pressure on USD reserve flows.

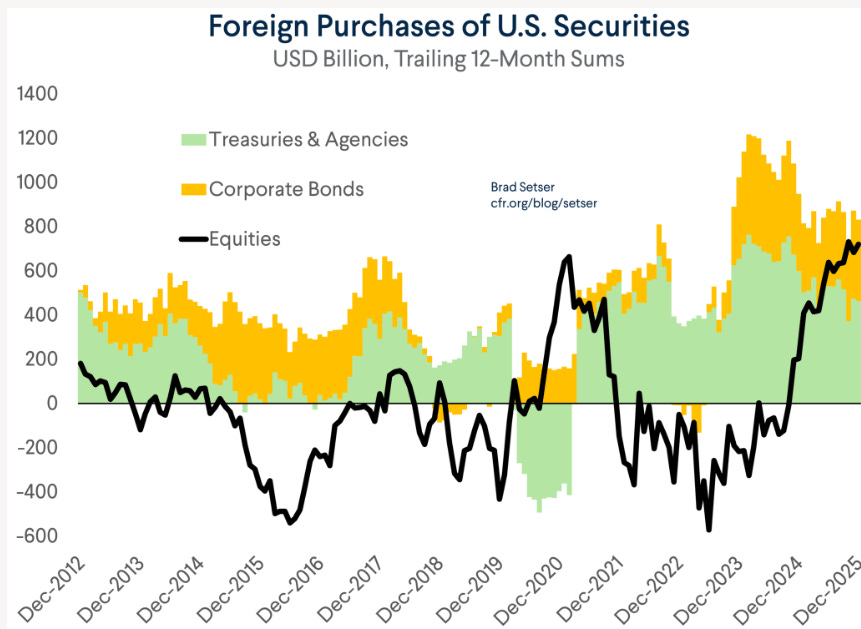

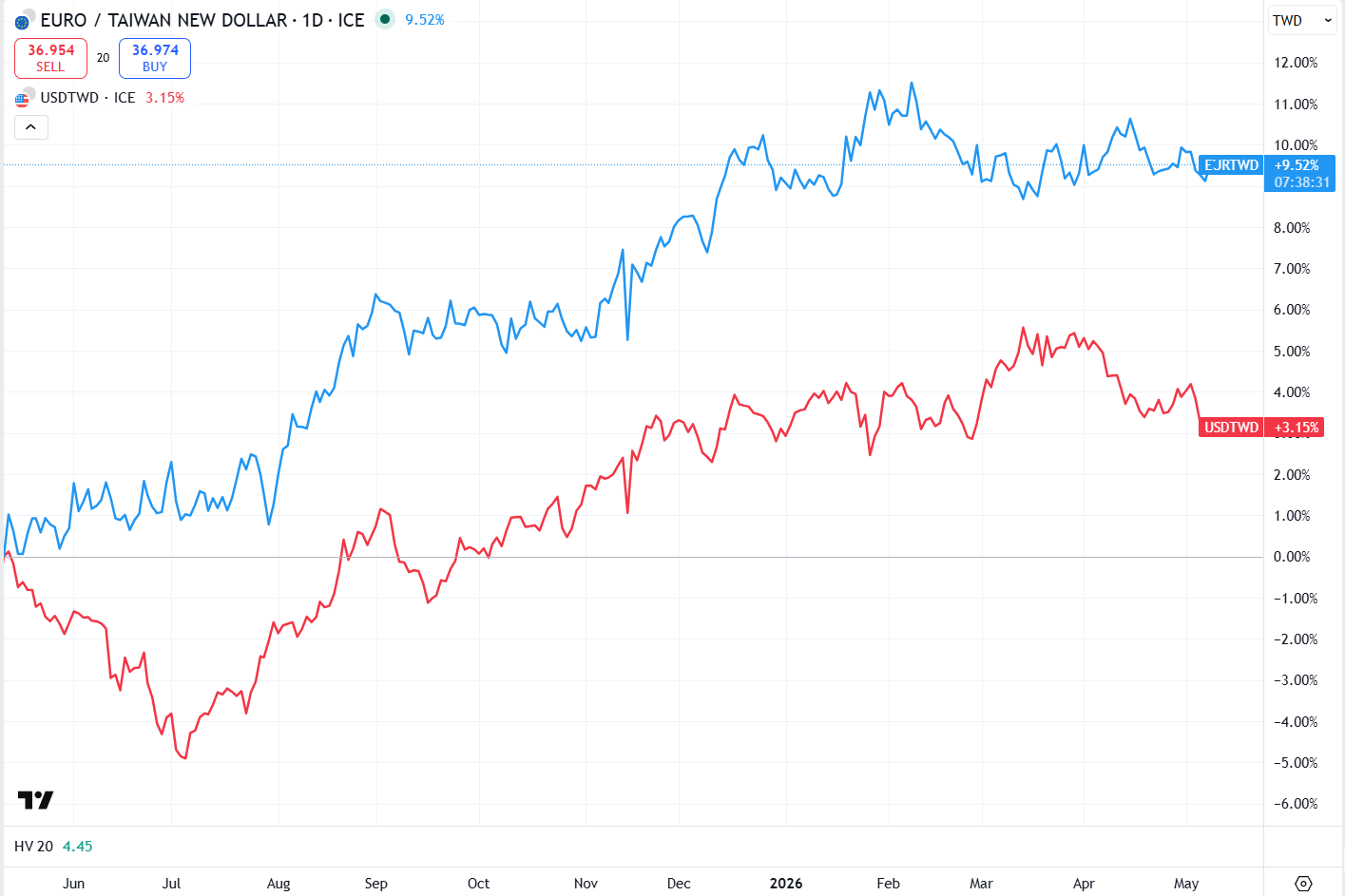

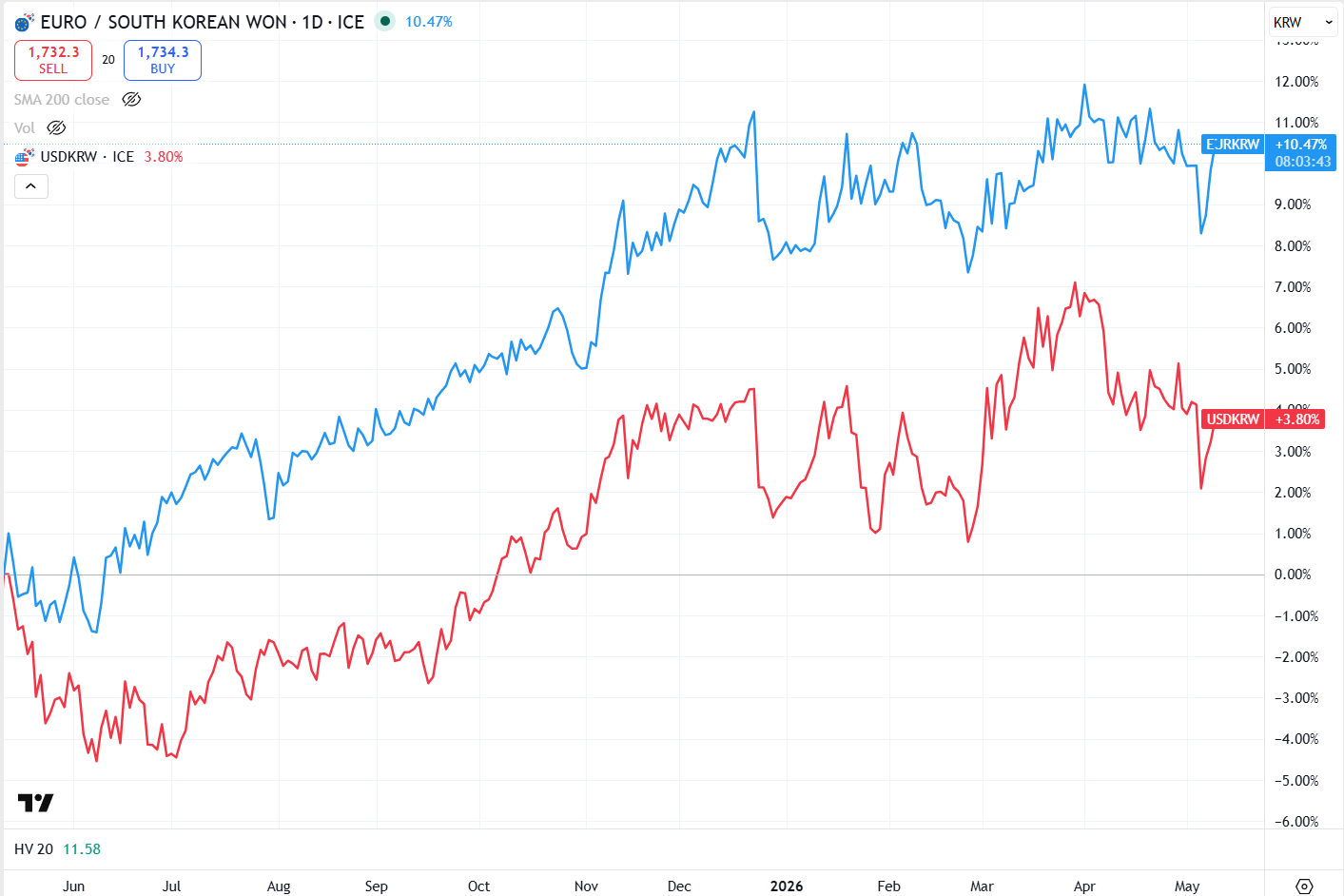

Foreigners are buying more US equities than bonds today which is historically unprecedented absent a brief disruption around COVID. This explains how we have stocks at all-time highs and yields hovering at local highs while the dollar languishes. Additionally, as European equities gain in popularity the Euro has outperformed the USD against the Taiwan dollar and South Korean Won which shows that foreign investors are increasingly favoring EUR equities over USD equities.

Which brings us to China and the upcoming meeting between Trump and Xi. With Taiwan becoming a critical element in the global AI supply chain and flow of dollars, the dispute between China and Taiwan gains a new dimension that becomes critical for the US. We speculated earlier that the US would be willing to offer China an accommodation over Taiwan as part of an understanding that would see China end its exploitation of the US market and agree to a balanced economic relationship, however now Taiwan could help China fill the gaping hole in their banking system and transition to credible reserve currency status.

It would be beyond ironic if the AI capex boom ended up helping to recapitalize China’s banking sector and advance its de-dollarization agenda. It would also demonstrate how the Chinese think on longer timelines than the West does. While the US exploits the incoherence of the anti-US alliance, China figures out how to turn it into an opportunity to trade Iran for Taiwan paving the way for its eventual emergence as an alternative reserve currency. The Campbell Ramble laid out how this might play out and while admittedly we don’t fully follow or agree with the reasoning, it is thought-provoking.

Besides, if we can see how the US is exploiting its adversaries then they are seeing the same thing and won’t be sitting by idly. Maybe the IRGC is backed into a corner and has limited options, and Russia is certainly signaling it is ready to move on from the Ukraine war and reintegrate into the global economy; but China is a different story. They aren’t just going to take US hegemony as a given. Despite their geographic vulnerabilities and banking system problems they are finding ways to maneuver around the US strategy and pick up wins where they can. The US and China are operating on different timelines as the US is a great power in decline and China is a rising power; therefore it is possible that China is willing to let the US win in the short-term by rebalancing their economic relationship to be more in favor for the US but to extract a long-term gain which increases China’s chances of displacing the US as the global reserve currency in the future.

Cedars Hill Group is a boutique investment bank built by investors. We invite you to explore our Knowledge Base to learn more about how you can run your business or portfolio like the best.

At CHG, we connect clients and experts to drive innovation and solve complex problems in today’s fast-paced and rapidly changing financial markets. Get in touch to learn how we can help you navigate your financial future.