CHG Issue #161: The Accordion

This is what happens when everyone tries to maximize their Sharpe

The cycles we experience in life and the markets are due to many factors which include some universal tendencies that have been observed by historians and philosophers since the beginning of recorded human history.

In "Discourse on the Origin of Inequality," Jean-Jacques Rousseau explores the transformation of human society from a state of natural equality to one marked by inequality and social disparity. He argues that in the state of nature, humans were solitary, self-sufficient, and motivated by basic needs and compassion. However, as society developed, the establishment of private property marked the beginning of inequality. This led to social institutions that perpetuated inequality through laws and governance favoring the wealthy. Rousseau critiques modern society for corrupting natural human goodness, suggesting that inequality is not a natural condition but a product of social evolution.

Alexis de Tocqueville identified a contradictory aspect of the equality of conditions in democratic societies. While equality fosters confidence and pride by making individuals feel equal to others, it also broadens the scope of comparison, leading to feelings of insignificance. In aristocratic societies, comparisons were limited to one's social class, but democracy removed those barriers, causing individuals to compare themselves to everyone. This results in overwhelming feelings of inadequacy and restlessness as individuals strive for unattainable equality. Tocqueville warned that this insatiable longing for equality could lead to societal instability and undermine the very democratic principles it seeks to uphold.

The universal theme here is the inability for anything in this world, anything we construct, whether physical good, thought, ideal, principle, or form, to deliver us from these cycles. Not only that but our very agitation for deliverance, whether that be in some absolute truth, or in certainty, is what undermines our efforts and subverts the foundation of society. Existence is a reflexive system where hidden feedback loops create unintended consequences that undermine our efforts.

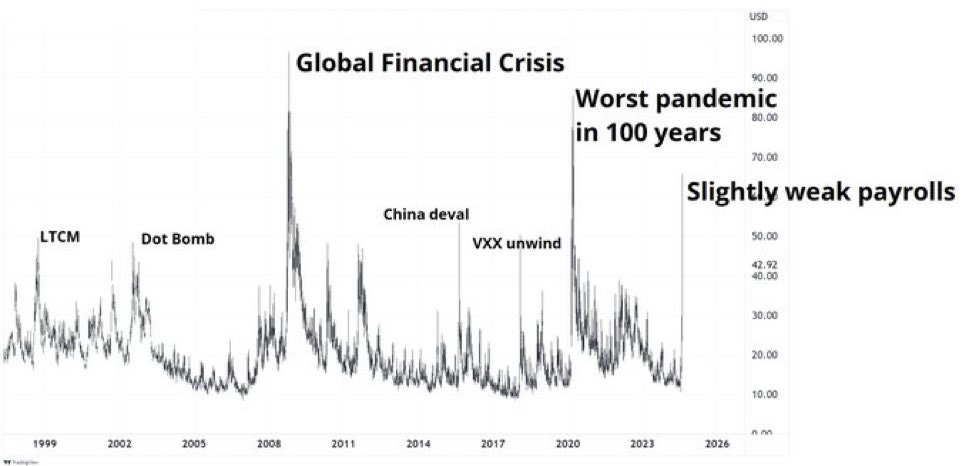

Taking the philosophical and applying it to the practical we can see a version of this playing out in recent market action. By trying to generate alpha by efficiently harvesting uncorrelated risk premia we have ended up creating a fragile market structure. Risk has to go somewhere; if everyone seeks to maximize their Sharpe ratio, there needs to be winners and losers for the game to remain zero-sum. The recent trend has been long the dollar, long tech stocks (growth), short small caps (value), and long alternative assets. As more money flows into those asset classes and strategies it lowers their expected return just like everyone betting on Kansas City to win the Super Bowl moves the betting line. As the competition in those asset classes increases investors pursue more granular and complex strategies that are inherently fragile due to their complexity. This dynamic gets exaggerated by the investment product marketing function which amplifies flows into popular asset classes and strategies that have "worked" recently. In The Third Law we wrote about how the flows from the dispersion trade were causing the market to entice you to bet on change which was the market's way of offlaying the risk from the dominant flows. Last week the chart below was being passed around which poked fun at the 65 VIX event we experienced on Monday morning. What we should see in this chart is not an over reaction to a payroll miss but the effect of a crowded trade being unwound (long tech - short small cap) which was identified well in advance of the 65 VIX event. The market was giving us good odds for something like this to happen so we shouldn't have been surprised when it happened.

Wall Street, and humans in general, have a tendency to take a good thing and pervert it by taking it to extremes. By dividing risk into more discrete units it allows that risk to be held by the investors best suited for that risk. However, at the same time that subdivision of risk creates new speculative vehicles with increasing complexity. Just like the ability to click on a button on your screen makes computers more functional it also creates additional complexity behind the scenes that an increasingly small subset of the population understands. Everything works well until the power goes out and no one knows how to get around without Google maps.

Minsky said stability is destabilizing and that may be one of the most enduring truths of human nature. We seek happiness and certainty, but anytime we find them they prove fleeting.

When the SIG founders started out they understood the implicit assumption of a right-skewed distribution of stock prices in the Black Scholes model and realized that stocks moved differently than that in the real world so they wanted to own the left tail of the distribution because they believed it was mispriced. That was edge and now that is widely known and we have put and call skew; as the options market evolved it got more sophisticated and efficient which means that edge is harder to find. You have to go to the dark corners of the market and look at things like the volatility-of-volatility, implied correlation, or spot-vol correlations to have a chance at finding edge.

As the performance of hedge funds and firms like SIG have bested that of traditional money managers more dollars have flowed into these managers and these strategies have grown. This makes the competition for edge more intense. It is still out there but to identify it and monetize it requires complex strategies. You might need to have several legs to your trade with each leg depending on the liquidity of that single market to extract edge and putting them on and taking them off in size becomes increasingly difficult.

Image an accordion as it expands and the amount of air it sucks in as a proportion of the total volume shrinks as it expands. This is the same dynamic in these "alpha harvesting" strategies. Risk is risk, no matter how many times you slice and dice it, but as you slice it into smaller units it creates opportunities for edge so the market is always expanding the accordion, pulling harder to get more air (edge) into the system but with increasingly less marginal return.

When the accordion can't expand any further it then compresses and the force of all that air comes out very violently at first. This is what we saw last week, the implied correlation trade had been pulled to far, partly due to the Mag 7 and Nvidia, that when it reversed it quickly caused a VIX 65 event.

Since the majority of investors today are price-takers when the accordion starts to reverse the price change required to accommodate the reversal of flows is exaggerated. Technology has mostly done away with traditional floor trading and as a result the number of true price-makers in the market has shrunk. Market makers today like SIG and Jane Street are huge firms, but still small in the grand scheme of the markets. Traditional market makers have mostly been replaced by algorithms run by firms like Citadel who is currently the largest market maker in the US. Banks have been out of the market making game for a while and they traditionally provided the ability to take the other side of the flows we saw last week which drove the 65 VIX event. The firms that took their place are not big enough or incented to provide a cushion to markets when risk gets re-priced which is why we see risk get re-priced in such a violent fashion like it did last week.